News

Audit thresholds in the Baltics

17 October 2016

The basic statutory audit threshold criteria for standalone financial statements of private companies in the Baltic countries are the same and comprise net sales, total assets and number of staff. However, the numbers in each country are quite different.

Audit

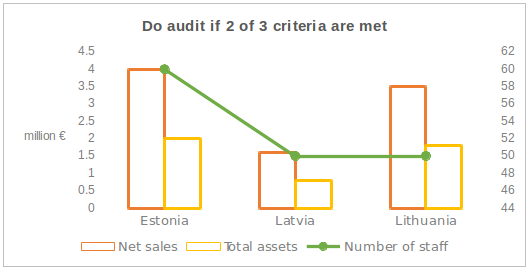

The chart below provides generic statutory audit threshold rules:

Further Latvia specific conditions are as follows:

- should you choose to measure and disclose items such as investment property, deferred tax, non-current assets held for sale, biological assets or any other asset or liability under IFRS, you will have to make an audit;

- should you have listed stock or debt, audit is a must;

- finally, should you have holding company, you must audit the accounts.

Review

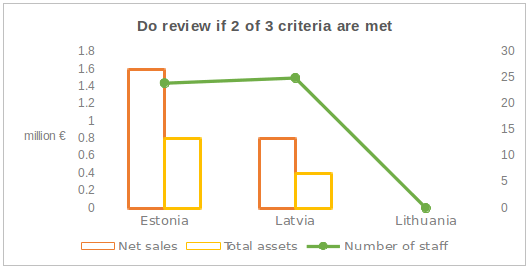

The following chart shows generic statutory review rules:

Further, in Estonia you will have to review your standalone accounts, should your net sales exceed €4.8m, total assets - €2.4m or headcount - 72 staff members.

What does above tell us?

- Latvia has the lowest audit thresholds in the Baltics

- In Latvia and Estonia you may be under obligation to arrange the review of accounts, whereas in Lithuania - you would not be

- We often hear that audit fees in Latvia are higher than in Estonia and Lithuania. This possibly to some extent is driven by lower audit thresholds.